For many people, a low credit score can feel like a significant barrier to securing a loan. Whether you’re looking to buy a car, start a business, or cover unexpected expenses, your credit score often determines the ease and terms of borrowing. While a high score opens doors to better rates and larger loan amounts, a low score doesn’t necessarily mean the door is closed. With the right strategies, you can improve your chances of securing a loan even if your credit score isn’t ideal.

Understand Your Credit Profile

The first step to securing a loan with a low credit score is understanding your credit profile. Request your credit report from the three major bureaus—Experian, Equifax, and TransUnion. By reviewing your report, you can identify the factors dragging down your score, such as late payments, high credit utilization, or inaccuracies.

Pay close attention to errors, such as accounts that don’t belong to you or late payments that you’ve already addressed. Disputing these inaccuracies with the credit bureaus can lead to immediate improvements in your score, enhancing your loan approval odds.

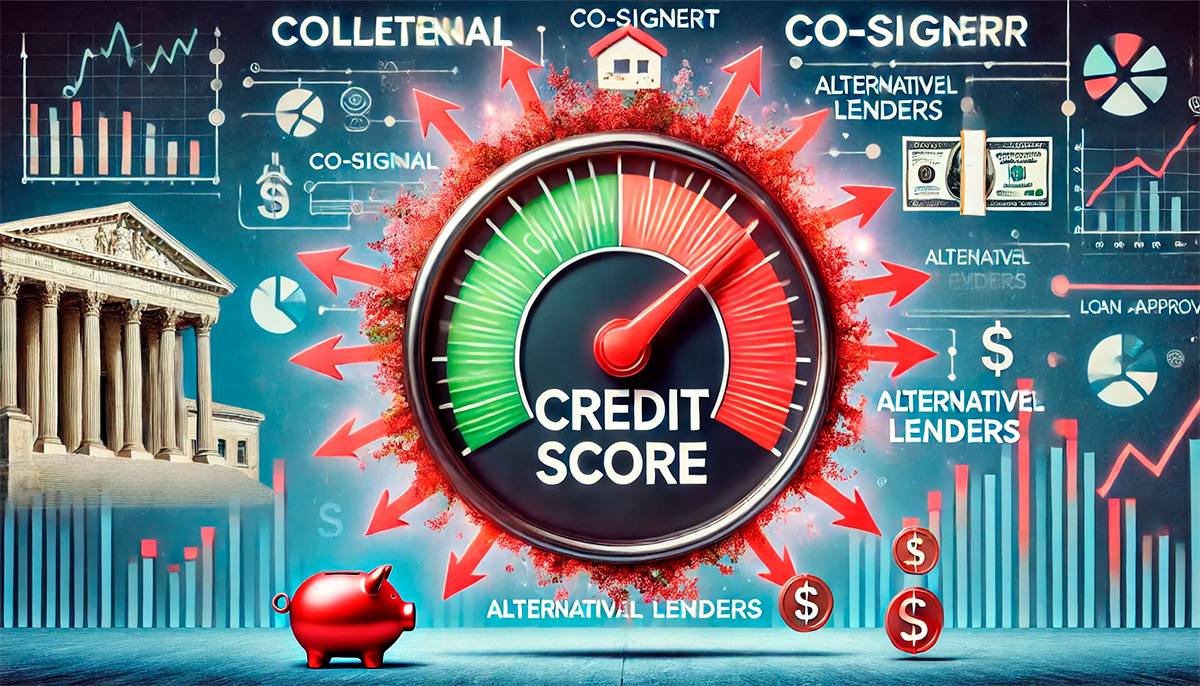

Consider Alternative Lenders

Traditional banks often have strict lending requirements, making it challenging for individuals with low credit scores to qualify for loans. However, alternative lenders, such as online loan providers, credit unions, and community banks, may offer more flexible options. These lenders often consider additional factors like income, employment history, and cash flow when evaluating applications.

For example, peer-to-peer lending platforms connect borrowers with individual investors who may be more willing to take a chance on someone with less-than-perfect credit. While these options might come with higher interest rates, they provide a viable pathway for those struggling to secure traditional loans.

Offer Collateral

Secured loans, which require collateral, can be an effective way to obtain financing with a low credit score. By offering an asset such as a car, home, or savings account as collateral, you reduce the lender’s risk, making them more likely to approve your application.

However, it’s essential to understand the risks associated with secured loans. If you fail to meet the repayment terms, the lender can seize your collateral. Before pursuing this option, ensure you have a clear repayment plan to protect your assets.

Provide a Strong Co-Signer

Enlisting a co-signer with a strong credit profile can significantly improve your chances of loan approval. A co-signer agrees to take responsibility for the loan if you’re unable to repay it, providing the lender with added security.

While this arrangement can help you qualify for a loan with better terms, it also places a significant responsibility on your co-signer. Be transparent about your financial situation and ensure both parties are comfortable with the arrangement before proceeding.

Focus on Improving Your Credit

While it may not be an immediate solution, taking steps to improve your credit score can enhance your borrowing prospects over time. Start by paying bills on time, as payment history is one of the most significant factors affecting your score. Reduce your credit utilization by paying down balances and avoiding new debt.

Additionally, consider opening a secured credit card or taking out a credit builder loan to establish a positive payment history. Even small, consistent improvements can have a significant impact on your credit profile over time, increasing your chances of securing future loans with better terms.

Demonstrate Financial Stability

Lenders are more likely to approve your loan application if you can demonstrate financial stability, even with a low credit score. Provide documentation showing a steady income, such as pay stubs, tax returns, or bank statements. Highlighting other financial assets, like savings accounts or investment portfolios, can also strengthen your case.

If you’re self-employed or have variable income, consider providing additional details about your business or cash flow to reassure lenders of your ability to repay the loan.

Apply for Smaller Loan Amounts

If your credit score is low, applying for a smaller loan amount may increase your chances of approval. Lenders are more likely to take a chance on borrowers with limited credit if the loan amount represents a lower risk.

Start with a modest loan that you’re confident you can repay. Successfully managing a smaller loan builds your credit history and improves your score, positioning you for larger financing opportunities in the future.

Prepare a Solid Loan Application

A well-prepared loan application can make a significant difference, especially when dealing with a low credit score. Take the time to gather all necessary documentation, including proof of income, a list of assets, and any letters of explanation for past financial challenges.

If your credit issues were caused by temporary setbacks, such as medical emergencies or job loss, explain these circumstances in your application. Lenders may view your situation more favorably if you can demonstrate that the issues were isolated and have since been resolved.

Negotiate Loan Terms

When dealing with lenders, don’t hesitate to negotiate the terms of your loan. While you may not qualify for the lowest interest rates, you can potentially secure better terms by offering a larger down payment, shorter repayment period, or additional collateral.

Building a relationship with the lender and demonstrating your commitment to repaying the loan can also work in your favor. Be open to discussing options that work for both parties and don’t be afraid to walk away if the terms aren’t favorable.

Use a Loan Marketplace

Loan marketplaces are online platforms that allow you to compare loan offers from multiple lenders. By filling out a single application, you can receive personalized loan options tailored to your financial situation. This approach increases your chances of finding a lender willing to work with you, even if your credit score is low.

Additionally, comparing offers helps you identify the most competitive rates and terms, ensuring you make an informed decision.

Conclusion: Persistence and Strategy Pay Off

Securing a loan with a low credit score is undoubtedly challenging, but it’s not impossible. By understanding your credit profile, exploring alternative lenders, and leveraging tools like co-signers or collateral, you can increase your chances of approval. Focus on demonstrating financial stability and preparing a strong loan application, and don’t hesitate to negotiate terms that work for you.

With persistence and the right strategies, you can overcome credit challenges and access the funding you need to achieve your goals. Start taking proactive steps today, and remember that every effort to improve your credit brings you closer to better financial opportunities in the future.